Monthly Economic Review for November 2015

- Details

- Category: Economic Release

- Created: 21 January 2016

Developments among Tonga’s key trading partners varied yet continued to support domestic activity. Growth in the US economy was revised up for September quarter driven by household consumption. Annual inflation in the US went up to 0.5% in November 2015 from 0.2% in October 2015. This is the highest rate in eleven months as energy costs declined at a slower pace in the US while prices of services increased slightly. Unemployment in NZ was particularly high despite a fall in unemployment rates in the US and Australia due to a surge in job growth. Oil prices fell significantly over the month of November 2015 from USD$48.56 to USD$44.86. The Tongan Pa’anga depreciated against both the Australian and the U.S. Dollar and appreciated against the New Zealand Dollar.

Domestic economic activities livened up over the month of November in preparation for the holiday season. Container registrations increased by 34.1%. Private container registrations increased by 46.3% while business container registrations increased by 30.2%. These indicate an active distribution and trade sector, both in the informal and formal parts of the sector.

An anticipated increase in tourism activities in the medium term is recognized to be a factor for the increase in vehicle registrations over the month. Vehicle registrations increased by 7.4% to a new record high mainly due to increases in “taxis and rentals” and “buses”. The Primary sector is also alive with agricultural exports about doubling over the month mainly due to further increases in squash exports.

Consumer price index declined over the month of November by 0.5%. This was mostly due to declining food prices (both domestic and imported) and the declining global oil prices. Lower domestic food prices included pineapples, ripe banana, and carrots whereas imported food prices included tinned and packaged foods as well as frozen meat. The price index for the domestic components fell by 1.0% while the imported components fell by 0.1%.

Over the year ended November 2015, headline inflation further declined by 1.9%. This was mainly due to a 4.7% decline in imported prices driven by declines in food and energy prices. This included most food such as ‘Fruit & Vegetables’, and ‘Meats, Fish & Poultry’. Domestic prices, on the other hand increased by 2.4% owing mostly to a 11.6% increase in domestic food prices. This was mainly driven by higher food prices for local ‘Fruit & Vegetables’ which coincides with lower annual agricultural exports due to El Niño weather conditions over the year. Despite the recent depreciation of the Tongan pa’anga against major currencies, the inflation rate has been well below the NRBT’s reference range for quite some time.

Although the Tongan Pa’anga (TOP) appreciated against the New Zealand Dollar (NZD), it’s depreciation against the US Dollar (USD) and the Australian Dollar (AUD) led to a slight decrease in the Nominal Effective Exchange Rate (NEER) of 0.1% followed by 1.0% decline in Real Effective Exchange Rate (REER). In annual terms, both the NEER and REER continues to depreciate as the TOP weakens against the USD, maintaining Tonga’s price competitiveness against that of its major trading partners.

Total Payments in Overseas Exchange Transactions (OET) further decreased in November by 10.0% to $44.1 million. Driving the fall was a 12.1% drop in Current account payments, and a 34.6% drop in Financial account payments, outweighing the slight increase in Capital account payments. Import payments were $5.6 million lower in November than the previous month, the largest contributor to the drop in current account payments. Despite a pickup in payments to imports of oil compared to the previous month, significant cutbacks were recorded in the payments for imports of wholesale & retail trade by $5.1 million. Tonga’s Foreign Exchange Levy Act 2015 that came into force on the 3rd of November after being deferred from the 21st of October, then later suspended on the 20th of November caused uncertainties amongst the financial institutions, hence the commercial banks reacted by restricting all foreign currency transactions coming in and going out of the country, contributing to the lower OET payments recorded for the month.

Total OET Receipts also fell by 31.1% over the month to $40.2 million. All major accounts decreased over the month with the financial account receipts decreasing the most by 77.2%. This was in the form of interbank transfers with its overseas correspondences which decreased over the month by $13.5 million, again reflecting the impact of the Foreign exchange levy imposed on the banks. Current accounts also decreased by 7.4%, largely driven by a 41.9% fall in travel services particularly in personal travel receipts. However, Export receipts increased over the month by $1.8 million showing improvements in proceeds from agricultural products specifically squash exports. Primary income receipts incurred a slight drop of $0.4 million due to lower receipts of pension and social receipts, whereas a decline in personal transfers led to the $0.3 million fall in transfer receipts.

Capital account receipts decreased by $1.9 million, as both official and private capital receipts which are mostly grants for investment projects, decreased over the month.

The balance of OET over the month of November, which is the net change to gross foreign reserves, recorded a surplus of $3.1 million, which is 24.4% lower than that in the previous month. The lower surplus coincides with a fall in the net financial account surplus of $11.9 million. Nevertheless, Gross foreign reserves reached a new record high of $319.0 million at the end of November, equivalent to 9.2 months of import cover, well above the NRBT’s minimum range of 3-4 months.

Broad Money slightly fell over the month by 0.2% to $427.8 million, due to a 2.2% decline in net domestic assets, offsetting a 0.6% rise in net foreign assets. The decline in net domestic assets was driven by a 2.2% rise in capital accounts particularly bank shares and other equity while the increase in foreign reserves explains the rise in net foreign assets. Bank deposits increased by 0.9% over the month attributed to a 3.7% and 1.5% growth in demand and time deposits respectively. Liquidity in the banking system slightly increased over the month by 0.3% to $171.1 million mainly due to an increase in banks’ settlements. Over the year, liquidity rose by 18.6% supported by a 15.8% rise in deposits.

Total bank lending over the month of November 2015 rose by 1.2%. This was due to increases in all lending categories particularly to household underpinned by increases in housing and vehicle loans. This coincides with the rise in the number of vehicle registrations and increased number of private house constructions currently on-going. At the same time, 33 new loans were approved from the managed funds scheme compared to 70 loans in October, totalling to about $0.26 million. Majority of these new loans were for new and existing customers in the manufacturing, trade and construction sectors. Including lending through the non-bank financial institutions credit growth only increased over the month by 1.1%, due to a decline in government on-lent loans.

Over the year, total bank lending rose by 12.0% driven by a 15.5% rise in lending to household with housing increasing the most. Banks lending to businesses also rose by 8.5% reflecting the increases in manufacturing, construction, tourism and agricultural loans. A decline in lending rate categories for these sectors supported the increase in lending over the year. Including lending offered by non-bank financial institutions, credit growth grew by 11.9%, reflecting the decline in government on-lent loans.

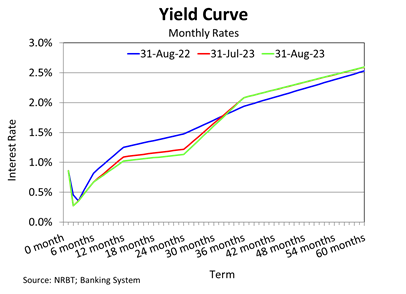

Weighted average lending rate slightly fell over the month to 8.07% from 8.09%. During the same period, the weighted average deposit rate also decline from 2.29% in October to 2.18%. This caused the weighted average interest rate spread to widen over the month from 5.80% to 5.90% in November 2015.

Net credit to government decline by 5% due to a 4% rise in government deposits. The increasing number of container registrations over the month reveal that customs collection also increased which support the rise in government deposits in November. In year ended terms, net credit to government fell by 18% driven by a 13% increase in government deposits due to receipt of budgetary support and project related grants from development partners.

Domestic economic activities remained broadly positive in the month of November. Tonga continue to benefit from global developments. Inflation remains relatively low given the low global oil prices. Monetary conditions improved as total credit and deposits continued to grow, and narrow weighted average interest rate spreads remains. Tonga’s financial system remains sound as the banking system continued to be profitable with strong liquidity and capital position being maintained. Consistent with the high banking system liquidity, broad money increased to its highest level and foreign reserves remained well above the minimum range. Given the above developments, the existing monetary policy setting is therefore considered appropriate in the near term.

The NRBT will continue to promote prudent lending, closely monitor credit growth and be mindful of the impact of a continued deflation. The NRBT will closely monitor the country’s economic developments and financial conditions to maintain internal and external monetary stability, promote financial stability and a sound and efficient financial system to support macroeconomic stability and economic growth.

Download the full review here.