Monthly Economic Review for February

- Details

- Category: Economic Releases

- Created: 27 April 2017

Economic growth in Tonga’s main trading partners continued to improve. This was due to stronger employment growth and some recovery in manufacturing output. The U.S., Australia and New Zealand maintained their accommodative monetary policy stance over February 2017. The U.S. Federal Reserve however indicated a continued tightening of its monetary policy. This was driven by positive economic growth, rising inflation, and high business confidence. The Reserve Bank of Australia (RBA) and the Reserve Bank of New Zealand (RBNZ) have, on the other hand, signalled that their official interest rates would remain on hold for some time. The outlook for these economies remain positive.

The domestic economy picked up after slow growth recorded in January, a similar trend to previous years. The agricultural sector improved due to a good harvest of root crops which outweighed the off season for fruits and vegetables during the month. This is evident in the increased prices of local fruits and vegetables in February 2017 by 23.6%. The agricultural exports volume rose by 182.8 tonnes (79.1%), largely due to a 155.5 tonnes (89.8%) rise in the volume of exported roots crops. The fisheries sector showed a mixed trend for its marine exports. The volume of fish exported over the month rose by 14.1 metric tons driven by a 17.1 metric tons increase in the volume of tuna exported. However, the export of all types of aquarium products decreased over the month by 3,264 pieces.

The secondary sector continued to grow strongly supported by the on-going construction works. Banks’ lending to the manufacturing sector rose by $0.5 million (3.1%), followed by an increase in lending to the construction sector of $0.5 million (5.0%) and loans to mining and quarrying grew by $0.1 million (25.6%). Similarly, the individual housing loans also increased by $1.8 million (1.1%).

The activities in the tertiary sector continued to reflect mixed growth. The distribution sector remained strong over the month as the number of container registrations rose by 243 registrations (37.6%) due to the increased volume of individual containers by 214 registrations (80.5%). On the other hand, vehicle registrations decreased by 32 registrations (11.2%) driven by lower privately licensed vehicles. However, the taxi & rental category rose by 15 vehicles over the month, which indicated probable growth in the transportation sector. International air arrivals also fell over the month by 33.4%, however the arrival of two cruise ships during the month may have supported the tourism sector.

The total number of job advertisements increased by 17 vacancies over February 2017 and also rose over the year by 40 vacancies, led by recruitment intentions in all the sectors particularly the services sector. This indicated a rising demand for labour in Tonga and may assist in reducing the unemployment rate.

| Monthly | Annual | |||

| Prices | Feb 17 | Jan 17 |

Feb 17 | Jan 17 |

| Headline Inflation (%) |

3.7 | 0.6 | 8.9 | 5.4 |

| Domestic prices |

6.3 | 1.3 | 6.8 | 2.4 |

| Imported prices |

1.8 | 0.2 | 10.5 | 7.7 |

Inflation rose over the month by 3.7% due mainly to a rise in domestic prices. The domestic prices increased by 6.3% mainly due to a 10.6% rise in prices of local food mainly prices of fruits and vegetables due to the seasonality of these food items. This was followed by a 12.1% and 6.3% rise in the price of electricity and kava-Tonga respectively. In addition, imported inflation rose by 1.8% over the month due to a rise in the prices of fuel, kerosene, liquid petroleum gas reflecting the increase in the global oil prices. The price of tobacco also increased by 7.5%, which was mainly due the higher price for Winfield blue cigarettes. Imported food prices rose by 0.9% for items such as mutton flaps, chicken pieces, sugar, and flour. This was due to the new custom duties and excise taxes introduced in July 2016 which drove the imported tobacco and food prices higher.

The annual inflation rate increased significantly by 8.9% in February 2017 compared to a 0.3% deflation in February 2016. This was largely due to a 10.5% increase in imported prices. During the same month last year, imported prices fell by 7.1%. However, the price of imported food, particularly meat, has been increasing since July 2016. Additionally, global food prices rose by 17.2% over the year. The price of tobacco has increased by 25.8% over the year due to new excise taxes. Moreover, the increase in world oil prices drove the price of fuel higher by 21.0%. This was followed by an increase in the prices of household supplies and services and house maintenance goods for items such as paint and bricks. Comparably, the domestic annual inflation rate rose by 6.8% largely due to the continued short supply of kava-Tonga and volatile local food prices. The price of kava-Tonga increased over the year by 71.4%, followed by a 9.0% increase in the price of local food, and a 5.4% increase in the price of domestic alcohol. Prices of electricity and household supplies & services also rose by 5.0% and 1.6% respectively.

| Monthly | Annual | ||||

| Feb 17 | Jan 17 |

% Growth | Feb 16 |

% Growth |

|

| Normal Effective Exchange Rate Index |

91.2 | 91.0 | 0.2 | 92.4 | -1.3 |

| Real Effective Exchange Rate Index |

104.9 | 101.1 | 3.8 | 99.2 | 5.8 |

In February 2017, the United States Dollar (USD), Australian Dollar (AUD), Chinese Yuan (CNY) and Japanese Yen (JPY) appreciated against the Tongan Pa’anga (TOP), while the New Zealand Dollar (NZD), Fijian Dollar (FJD), Euro Dollar (EUR) and British Pound (GPB) depreciated against the TOP. As a result, both the Nominal Effective Exchange Rate (NEER) index and the Real Effective Exchange Rate (REER) index slightly increased over the month. In annual terms, the NEER index continued to fall while the REER index rose. The rise in the REER index reflected Tonga’s higher headline inflation rate relative to its trading partners, which may impact the international competitiveness of the Tongan exports of goods and services.

| Monthly | Annual | ||||

| Feb 17 | Jan 17 |

% Growth | Feb 17 |

% Growth |

|

| OET Receipts (TOP $ million) |

44.8 | 57.5 | -22.2 | 736.0 | 23.8 |

| Export receipt |

1.5 | 2.2 | -30.2 | 22.1 | 46.1 |

| Travel receipt | 6.0 | 10.0 | -39.6 | 100.1 | 24.3 |

| Private transfers | 17.5 | 20.4 | -13.9 | 251.3 | 17.2 |

| Others | 19.6 | 24.9 | -21.2 | 362.5 | 27.6 |

| OET Payments (TOP $ million) | 45.9 | 42.8 | 7.2 | 616.9 | 16.4 |

| Import payments | 21.0 | 26.0 | -19.2 | 344.1 | 12.2 |

| Services payments | 13.5 | 10.0 | 35.5 | 143.7 | 28.8 |

| Primary Income payments | 0.5 | 0.6 | -14.8 | 23.6 | 50.9 |

| Others | 10.8 | 6.2 | 74.4 | 105.5 | 9.9 |

Total OET receipts continued to decline over the month of February 2017, by 22.2% to $44.8 million. This was mainly driven by a decline in direct investment receipts, following a large receipt of $7.1 million last month. Travel receipts also fell mainly due to lower personal travel receipts which coincided with the decline in the international air arrivals. On year ended terms, total OET receipts however rose by 23.8% which was largely owing to the higher inflows of private remittances and official grant receipts. Majority of the remittance receipts were in USD which was supported by the depreciation of the TOP against the USD. The AUD and NZD receipts followed which were supported by the weakening of the TOP against these currencies. This coincided with the positive economic growth in these countries.

In contrast, total OET payments slightly increased in February 2017 by 7.2% to $45.9 million. This was a result of higher payments for services particularly repatriation of airline tickets to their respective overseas head-office.

Total OET payments also rose over the year by 16.4%, which was driven by higher imports, mainly payments for wholesale & retail imports, as well as payments for services and primary income payments.

| Monthly | Annual | ||||

| Feb 17 | Jan 17 |

% Growth | Feb 16 |

% Growth |

|

| Foreign Reserves ($ in million) |

377.7 | 380.8 | -0.8 | 328.5 | 15.0 |

| Import Coverage (months) |

7.1 | 7.2 | 7.1 | ||

The overall balance of OET for February 2017 was therefore a deficit of $3.2 million. This contributed to the decrease in the official foreign reserves to $377.7 million in February 2017, equivalent to 7.1 months1 of imports cover, which is still above the Reserve Bank’s minimum range of 3-4 months.

Broad money (money supply) fell over the month due mainly to the lower foreign reserves resulting in lower net foreign assets. This outweighed an increase in net domestic assets which was driven mainly by the increase in net domestic credit and also the decline in deposits over the month. However, broad money continued to show strong growth over the year largely as a result of higher foreign reserves.

| Monthly | Annual | ||||

| Money | Feb 17 | Jan 17 |

% Growth | Feb 16 |

% Growth |

| Money Supply ($ in million) |

510.2 | 512.0 | 0.4 | 456.5 | 11.8 |

| Net Foreign Asset |

390.8 | 407.1 | -4.0 | 330.3 | 18.3 |

| Net Domestic Asset |

108.3 | 105.1 | 3.0 | 126.5 | -14.4 |

The liquidity (reserve money)2 in the banking system slightly decreased over February by $2.3 million (0.8%) due to higher cash withdrawals by the commercial banks from the Reserve Bank vault during the month. This largely reflected the Reserve Bank’s efforts to replace mutilated notes in circulation with new banknotes issued to the public. This would in turn ensure that good quality banknotes and coins are in circulation. Furthermore, banks’ total loans to deposit ratio rose over February to 73.3% from 72.4% in January, driven by the decline in deposits as well as the credit growth over the month. The lower deposits in February coincided with the fall in the foreign reserves and rise in net domestic assets. The loans to deposit ratio of banks remained below the 80% minimum loan to deposit ratio target which indicated excess liquidity in the banking system remains and that more capacity for further lending by the banks exists.

| Monthly | Annual | ||||

| Lending | Feb 17 | Jan 17 |

% Growth | Feb 16 |

% Growth |

| Total Lending ($ in million) |

384.5 | 382.2 | 0.6 | 331.9 | 15.9 |

| Business Lending |

165.5 | 166.3 | -0.5 | 155.4 | 6.5 |

| Household Lending |

217.9 | 214.8 | 1.4 | 175.3 | 24.3 |

| Other Lending | 1.1 | 1.1 | 0.5 | 1.2 | -9.2 |

Lending by banks rose over February and over the year driven mainly by increased lending to households. Housing and other personal loans contributed significantly to the overall credit growth. Vehicle loans also increased. This is indicative of high borrower capacity and demand by individuals. In contrast, lending to businesses declined over February owing largely to lower lending to the professional services, tourism and utilities sectors. However, over the year, higher lending to tourism, agricultural, manufacturing and construction sectors resulted in a 6.5% increase in total business loans. The lower interest rates from the Government Development Loans partially supported the higher lending to these sectors. Credit growth was $52.6 million (15.9%) over the year to February, which exceeded the $34.5 million (11.6%) growth in the year ended February 2016.

| Monthly | Annual | ||||

| Money | Feb 17 | Jan 17 |

Growth (bps) |

Feb 16 |

Growth (bps) |

| Weighted Average Banks Deposit Rate (%) |

2.213 | 2.177 | 3.6 | 2.190 | 2.3 |

| Weighted Average Banks Lending Rate (%) |

7.913 | 7.881 | 3.2 | 8.028 | -11.5 |

| Weighted Average Interest Rate Spread (%) |

5.700 | 5.704 | -0.4 | 5.839 | -13.9 |

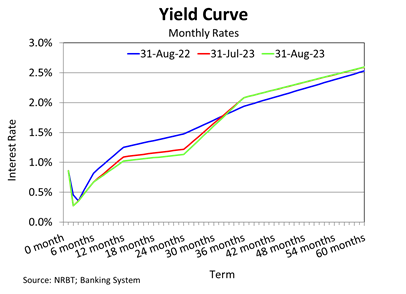

The weighted average interest rate spread narrowed slightly in February to 5.7% mainly due to an increase in the weighted average deposit rate which outweighed the rise in the weighted average lending rate. Business lending rates increased over the month, particularly for the manufacturing, construction and distribution sectors. The weighted average deposit rate increased due to higher term deposit rates. Similarly on an annual basis, the weighted average interest rate spread narrowed by 13.9 basis points driven by a fall in the weighted average lending rate and an increase in the weighted average deposit rate. Lower lending rates to businesses and households led to a decline in the overall weighted average lending rate. More specifically, housing lending rates decreased and similarly, the lending rates for the agricultural, utilities and tourism sectors also declined over the year. This also coincided with higher credit growth recorded over the year. In contrast, the increase in demand and term deposit interest rates resulted in the rise in the weighted average deposit rate.

Net credit to Government rose over the month by $1.0 million, due to a decline in government deposits due to higher payment obligations during the month. Net credit to government however fell over the year which stemmed from rising government deposits due to the receipt of budgetary support funds during the year.

The Reserve Bank’s outlook for strong domestic economic activity remains in the medium term. The level of foreign reserves is also expected to remain at comfortable levels supported by expected higher receipts of remittances and foreign aid and this will be partially offset by the projected rise in imports. Upward inflationary pressure remains in the near term due to the impact of the increase in custom duty and excise tax effective on 1st July 2016, however it is expected to fall below the Reserve Bank’s inflation reference rate of 5% per annum in 2017/18. In light of the above developments and that the banking system remained sound, the Reserve Bank Board maintained its current accommodative monetary policy measures. The Reserve Bank will continue to closely monitor developments in the domestic and global economy, and update its monetary policy setting to maintain internal and external monetary stability, and to promote a sound and efficient financial system in order to support macroeconomic stability and economic growth.

1 - Methodology used for this calculation has changed to include both imports of goods and services whilst the calculation used in previous reports used import of goods only

2 - Sum of currency in circulation, exchange settlement account balances, and required reserve deposits.

Download the full review: Monthly Economic Review - February 2017