Monthly Economic Review for January 2016

- Details

- Category: Economic Release

- Created: 30 March 2016

Global growth prospects for 2016 deteriorate due to uncertainties surrounding the health of the Chinese economy. Japan has lowered its benchmark interest rate to -0.1% in order to stimulate economic activity. A cutback in business investments and loss of jobs from the energy sector in the US, along with the stronger US dollar is indicative of a potential recession. Australia’s construction activities increased in December 2015, and the unemployment rate fell to 5.8% from 6.2%. NZ also showed improvement as GDP is projected to advance by 2.4% in 2016 and 2.8% in 2017, whilst unemployment rate dropped from 6.0% to 5.3% in the fourth quarter. For 2015 as a whole, inflation averaged 1.5% and 0.3% for Australia and NZ respectively, both recording their lowest reading since 1999. World oil prices dipped below USD$30 a barrel in the latter part of January but again rose to USD$34.28 at the end of the month.

Overall economic activity in January 2016 showed a downturn following a busy month with Christmas festivities and other events. The primary sector slowed which was supported by an increase in domestic food prices reflecting lower primary production. Agricultural exports volume also continued to fall over the month of January by 67.8% to 171.7 tonnes. This is mainly due to a decrease in exports of all major products except vegetable products. Tropical Cyclone Ula that occurred during the month also contributed to the lower agricultural production. Banking data showed proceeds for the export of agricultural products declined by 78.1% marking the end of the squash season. Proceeds for the fisheries exports however rose by 44.4%.

The services sector also weakened over the month. The end of the festive and holiday season resulted in a significant drop in total container registrations in January by 48.8%. This is driven by a decrease in both business and private container registrations. The decline in international arrivals by 28.3% impacted the activities in the hotels and restaurants sector. This coincided with a fall in travel receipts of $0.5 million over the month. Domestic fuel prices remained constant which buoyed the transport sector while vehicle registrations recorded a decline of 25.9%. Activities in the financial sector were supported by higher credit growth during the month.

The secondary sector however remained strong. Increases in individual housing loans and business loans for construction and manufacturing also supported the expansion of the secondary sector.

Indication of lower unemployment over the month is implied by the decline in the total number of job advertisements1 compared to December 2015. The Public Sector continued to record the highest number of vacancies advertised and the Ministry of Education remained the main contributor reflecting the new recruitment for the start of the academic year. Over the year, job advertisements also fell by 22% driven by lower number of job advertisements for the Industry and Primary sectors.

Higher domestic prices for Miscellaneous goods & services, Tobacco & Alcohol and Household operations pushed up the headline inflation over the month by 1.9%. Prices for Miscellaneous goods & services rose by 24.9% as a result of higher stamp prices for air mail to Australia. Tobacco & Alcohol prices also rose by 5.0% driven by an increase in prices for alcohol. Household operation prices rose by 4.6% due to increases in the prices of equipment & utensils, furnishing and textiles. Food prices rose by 2.6% due to increases in the prices of ripe banana, capsicum, taro leaves, cucumber, string fish, clamp and frozen fish. Imported prices however, continued to fall by 0.5% over the month as a result of a 2.6% decline in prices for petrol and diesel offsetting a 4.9% rise in the price of Clothing & footwear as increased demands from preparation for the commencement of the school year contributed to an increase in prices of school uniforms.

Annual headline inflation rate continued to fall by 1.3%. This was mainly due to a 6.7% decline in imported prices driven by a decrease of 11.6% in prices for food items such as potatoes, onions, mutton flaps and chicken pieces. A decline in prices of crude oil were reflected in the fall in prices of transportation by 6.1%. Household operation prices also declined by 5.9% due to lower prices of domestic fuel and power. Domestic prices however rose by 6.4% reflecting increases in stamp prices for air mail contributing to a 24.9% rise in prices for Miscellaneous goods & services. Higher prices for ripe banana, taro, yam, cassava and sweet potatoes contributed to an increase in food prices by 10.2%. The National Reserve Bank of Tonga (NRBT) continues to expect that headline inflation will remain low in the near term. However, risks to this forecast would be developments in world oil and food prices for both domestic and imported inflation.

In January, the Tongan Pa’anga strengthened against the New Zealand, Australian and British Pounds, but weakened against the US dollar, Fijian dollar, Chinese Yuan, Japanese Yen and Euro. As a result, the Nominal Effective Exchange Rate (NEER) fell over the month by 0.04%. However, the Real Effective Exchange Rate (REER) rose by 1.47% due to the relatively higher monthly headline inflation for Tonga relative to Tonga’s trading partners. In year-ended terms, both the REER and the NEER fell at a faster rate of 10.6% and 5.3% respectively.

The total Overseas Exchange Transactions (OET) payments for the month of January fell by 4.2% to $42.8 million, mainly due to a 3.5% decline in current account payments. Service payments fell by 17.5% mostly owing to lower payments for telecommunication, professional and business services recorded for the month, which more than offset a 1.4% rise in import payments mainly for oil.

Total OET receipts fell significantly over the month by 34.2% to $39.1 million. Receipts in all major accounts have declined with the current account receipts declining the most by $15.2 million due to transfer receipts dropping by 37.0% over the month. Since the Christmas season is now over, remittances receipts have dropped by $8.9 million along with the receipts of official grants for technical assistance and other current expenditures by $3.6 million. Total export receipts fell by 52.3% to $1.0 million which are mostly from agricultural exports. Services receipts also fell by 17.7% due to lower travel, construction, professional & business, and other services receipts. Despite an increase in the form of interbank transfers during the month, the financial account receipts still declined from last month due to lower fund transfers by resident businesses and non-profit organisations from their deposits in non-resident banks to Tonga. The decline in capital account receipts was due to lower receipts of official grants for capital expenditures offsetting the rise in private capital transfers.

In January, the balance of overseas exchange transactions, which is the net change to foreign reserves, was a deficit of $1.6 million relative to a surplus of $8.8 million recorded in December 2015. This turnaround was a result of higher net current account outflow of $8.4 million underpinned by lower transfer receipts, thus contributing to the fall in official foreign reserves to $326.3 million at the end of January. This is equivalent to 9.5 months of imports cover, well above the NRBT’s minimum range of 3-4 months.

Broad money slightly fell over the month by 0.6% to $447.5 million, due to a 0.7% decline in net foreign assets, and a 0.4% fall in net domestic assets. The lower net foreign assets resulted from a 0.4% decline in foreign reserves whilst a 27.3% decline in other items (net) driven by an increase in miscellaneous liability items explains the decrease in net domestic assets. However, liquidity in the banking system increased over the month by 3.2% to $174.7 million which was supported mainly by an increase in banks’ deposits of proceeds from the sales during the festive season to the NRBT vault. This coincides with a 9.5% fall in currency in circulation over the month.

Total bank lending increased slightly over the month by 1.1% to $328.9 million. Bank lending to both businesses and individuals increased with business loans rising by 1.3% and household loans growing by 0.6%. The increase in business loans was mainly due to rises in lending to the manufacturing, tourism and trade sectors. Consecutive rises in housing loans on the back of competitive housing loan interest rates have continued to drive household loans to another high record, suggesting consumer confidence remain strong. Including loans extended by non - banks, total lending increased by 1.0% underpinned mainly by increases in household loans. Over the year, total bank lending rose by 12.4%, due mainly to increased lending to households.

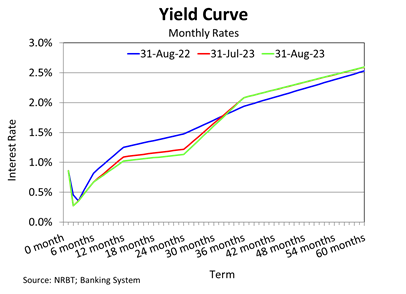

Weighted average lending rate fell over the month by 2.8 basis points to 8.04% while weighted average deposit rate rose by 3.6 basis points to 2.19%. As a result, weighted average interest rate spread narrowed over the month from 5.92% to 5.85% in January 2016.

Net credit to government slightly rose over the month by 2.3% due to a 4.9% rise in government deposits reflects a continued rise in government revenue collection. During the month there were new bond issued of $7.7 million, which resulted in a 24.1% rise in banks’ bond holdings. Over the year to January, net credit to government rose by 11.0% driven by a 2.1% decline in government deposits as government clears its commitments and payments obligations.

Against the background of continued deflation, foreign reserves remaining comfortably above the minimum range of 3-4 months of import cover, positive credit growth and the banking system remaining sound, the current monetary policy stance remain appropriate in the near term, which is consistent with the recent assessment by the 2016 IMF Article IV mission2. Nevertheless, the NRBT is considering measures to ensure the excess liquidity in the banking system are being well utilised to support economic growth. At the same time, the NRBT is exploring alternative monetary policy tools and macroprudential tools to strengthen the transmission mechanism and ensure financial stability is maintained. The NRBT will closely monitor the country’s economic and fiscal developments and financial conditions to maintain internal and external monetary stability, and promote a sound and efficient financial system to support macroeconomic stability and economic growth.

Download the full review here.

1 - This is based on job advertisements published on local newspapers (Taimi, Talaki and Kele’a) and the Matangi Tonga Website).

2 - IMF Article IV Mission to Tonga 2016, Press Release No. 16/97, Dated 10th March 2016.